The Next Investment Super-Cycle Is a Balance-Sheet Event

The world is about to spend on the order of $16 trillion a year building the future. The interesting question isn't what gets built — it's who finances it, and through what plumbing.

Florian M Spiegl

Founder & CEO

Published

June 10, 2026

A large part of our work is forming a house view on what lies ahead and where capital should focus next. For months, one question has sat at the centre of that research, and it keeps returning the same answer: we are at the beginning of a new investment super-cycle, not the end of one.

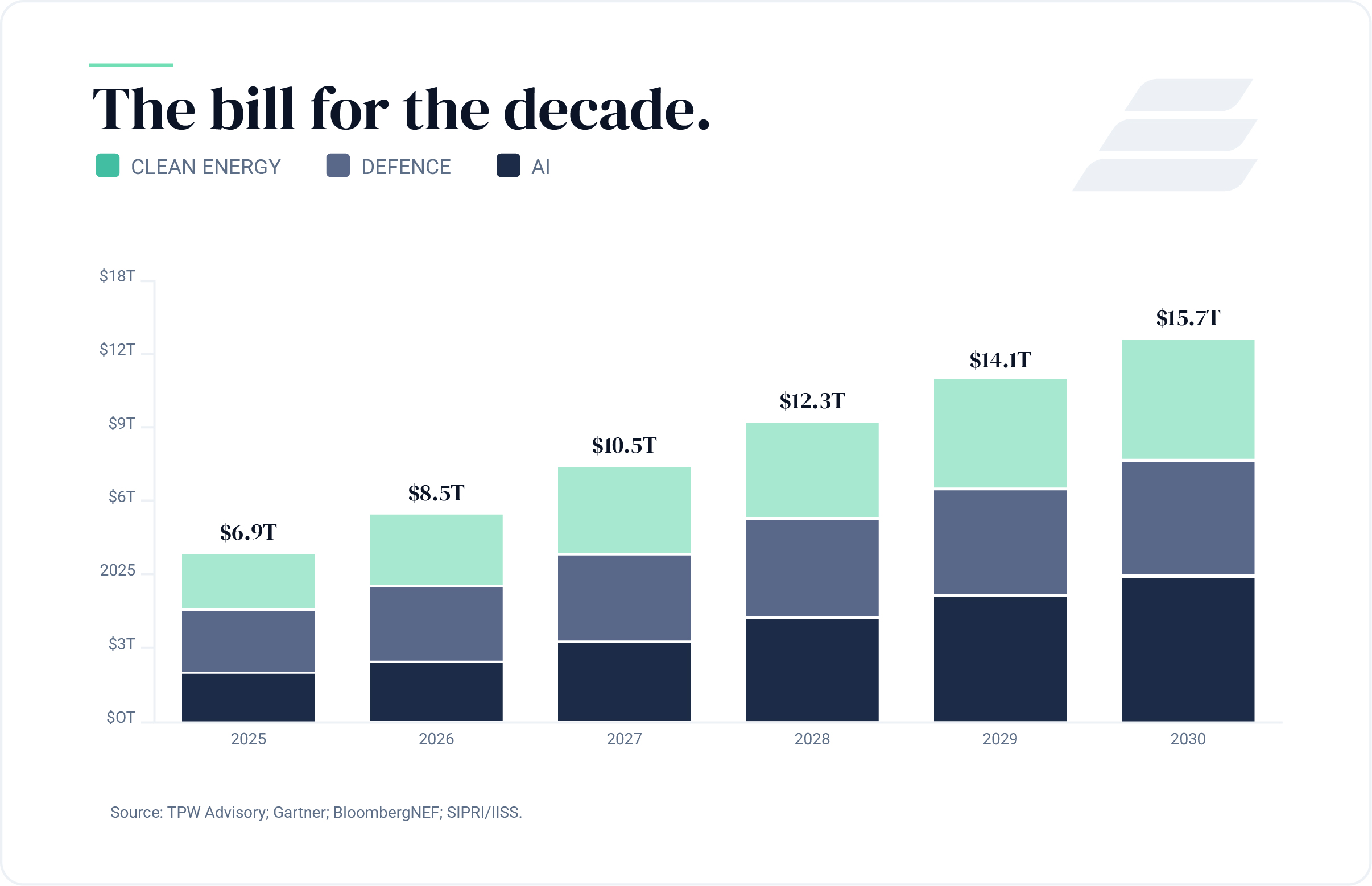

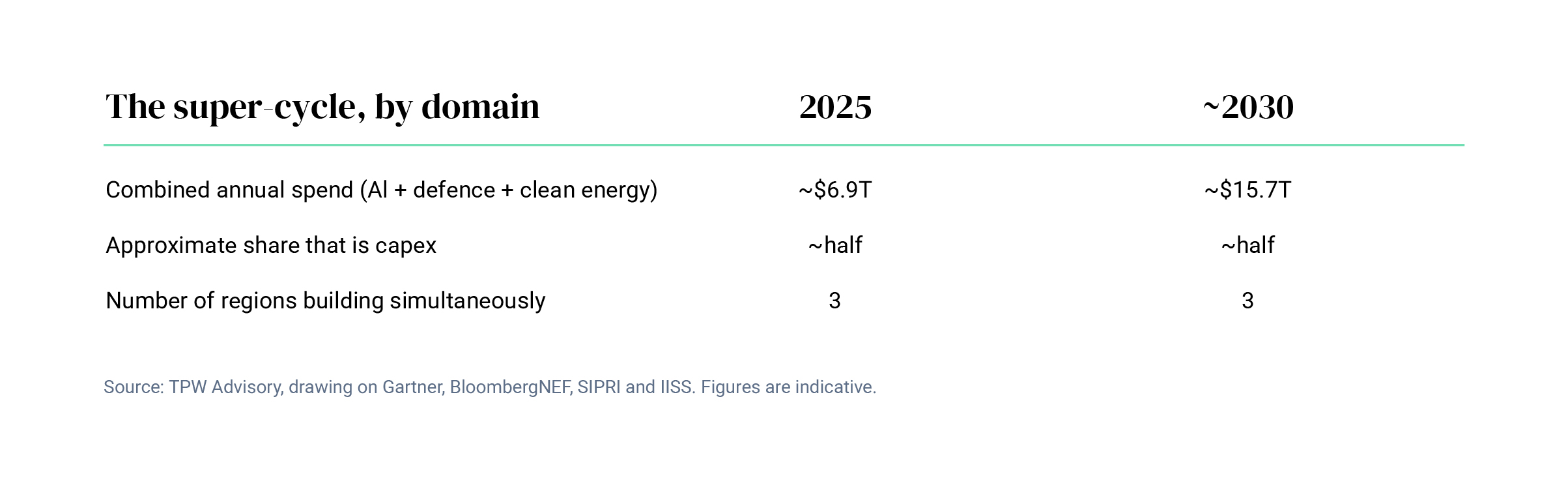

The shape of it is now widely described. Over the next five years the world will spend on the order of $16 trillion a year building three things at once — artificial intelligence, defence, and clean energy. According to TPW Advisory, which aggregated the forecasts from Gartner, BloombergNEF and the defence trackers, the combined figure was roughly $6.9 trillion in 2025, is already close to $10 trillion this year, and is on track for around $16 trillion by 2030. The novelty is not any single line item. It is the breadth: three domains, three regions — Asia, Europe, the Americas — reinforcing one another at the same time. Nothing of this scale and synchrony has happened in living memory.

That much is becoming consensus. What follows is the part most of the commentary skips, and it is the part that matters most for anyone allocating capital. This is a financing event before it is a stock-picking event. Once you see it that way, the super-cycle stops being a public-markets story and becomes, to a surprising degree, a private one.

A spending event is a financing event

Roughly half of that $16 trillion is capex — real, long-lived assets, not earnings or multiples. Power generation and grids, data centres, fabrication plants, mines, processing facilities, ships. Things that are built once and owned for decades, and that sit on a balance sheet the entire time they exist.

This is the distinction the headline numbers obscure. A spending super-cycle of this composition is, mechanically, a capital-expenditure cycle — and a capital-expenditure cycle is a financing problem long before it is an investment theme. The former Goldman commodities strategist Jeff Currie puts the underlying logic plainly: the price spike everyone watches is the symptom; the disease is years of capex starvation. Closing that gap requires building the physical layer of the economy back up — and physical assets have to be funded, owned, and held.

It helps to picture the spend as a stack. At the bottom sits energy; above it, chips; above that, the physical infrastructure — data centres, grid, cooling, networking; and only at the top, the models and applications that capture most of the public's attention. The last technology cycle rewarded the top of that stack: capital-light software businesses that captured margin while capital recycled frictionlessly across borders. This cycle inverts the picture. The value, and the scarcity, are migrating down — to the heavy, capital-intensive base. The phrase doing the rounds among the people building it is blunt: your capex is my opportunity.

The scale at the base is hard to overstate. Data-centre capital expenditure alone has run to roughly $930 billion over six years and, on McKinsey's estimate, could reach about $3 trillion between 2025 and 2030 — a single category outspending the Interstate Highway System and the Apollo programme combined, compressed into a fraction of the time. These are not assets you gain exposure to by buying an index. They are built, financed, and owned — one balance sheet at a time.

From global and liquid to heavy and local

The deeper shift is a change of regime: from an economy of light, globally-mobile capital to one of heavy, locally-anchored assets. Currie's shorthand captures it — the old model was hard assets, global operations; the new one is heavy assets, local operations. Capital that once moved frictionlessly across borders is now being committed to physical things, built close to where they are consumed, with long lead times and long holding periods.

The reindustrialisation data tells the same story from another angle. McKinsey estimates the United States imports about $3 trillion in manufactured goods a year, of which roughly a quarter are strategically exposed — critical, concentrated in a few suppliers, and sourced from geopolitically distant partners. Rebuilding the domestic capacity to produce those exposed goods and their upstream inputs could require on the order of $2 trillion in capital expenditure — around 6 percent of GDP. And the capital is already concentrating into large commitments: deals above $1 billion now account for more than 70 percent of announced foreign direct investment into US manufacturing, up from roughly a third before the pandemic.

This is what the Bank of America strategist Michael Hartnett means when he argues that the decade's organising principle is to own what is in scarce supply. Scarcity has moved. For a generation it sat in the intangible and the digital. It is migrating to the tangible and the physical — energy, grid capacity, critical minerals, processing, the industrial base itself. Those are not public-equity abstractions. They are real assets with real cash flows, owned by someone.

In our own language, the world is moving from a stock business to a flow business: from large positions that sit, to assets that are built, financed, traded, and refinanced. The macro regime and the structure of private markets are converging on the same shape.

The constraint is not capital

Here is the counterintuitive heart of it: there is more money looking for these assets than there are efficient ways to move it into them.

Consider the abundance. US households held a record $68 trillion in equities at the end of 2025 — the highest share of household wealth on record. A further $8 trillion sits idle in money-market funds. The value of financial assets relative to GDP is at an all-time high. New vehicles are being raised specifically to fund the build: Jeff Bezos is reportedly assembling up to $100 billion for a manufacturing-automation fund; others are following. When McKinsey modelled what reindustrialisation would actually require, it reached a conclusion that should reframe the entire debate: the funding would be the easy part.

The hard part is everything around the money. In the real economy, the binding constraints are skills, energy, permitting, and shovel-ready projects — not dollars. And in the financial economy, the constraint is structurally similar: the difficulty is not raising capital but channelling it — getting it into the right assets, and engineering the liquidity that lets an investor commit to something illiquid in the first place.

This is the gap we spend our days inside. The capital exists. The rails to move it into these assets — at the speed, in the sizes, and on the terms that private capital requires — largely do not. Subscription processes still run on forty-page documents and manual signatures; identity and suitability checks are rebuilt for every new relationship; positions are reconciled on spreadsheets; reporting arrives quarterly, if at all. For a pension fund writing a $200 million cheque, that friction is a rounding error. For a family office allocating $2 million, or a private bank building an alternatives shelf for two hundred clients, it is prohibitive.

The money leg, not the money, is the real bottleneck of the decade.

Why this becomes a private-markets story

The assets being financed are heavy, local and long-dated — the native territory of private capital — and they offer a fundamentally different return engine. This is the conclusion the financing lens forces, and it is worth stating precisely, because it is often argued badly.

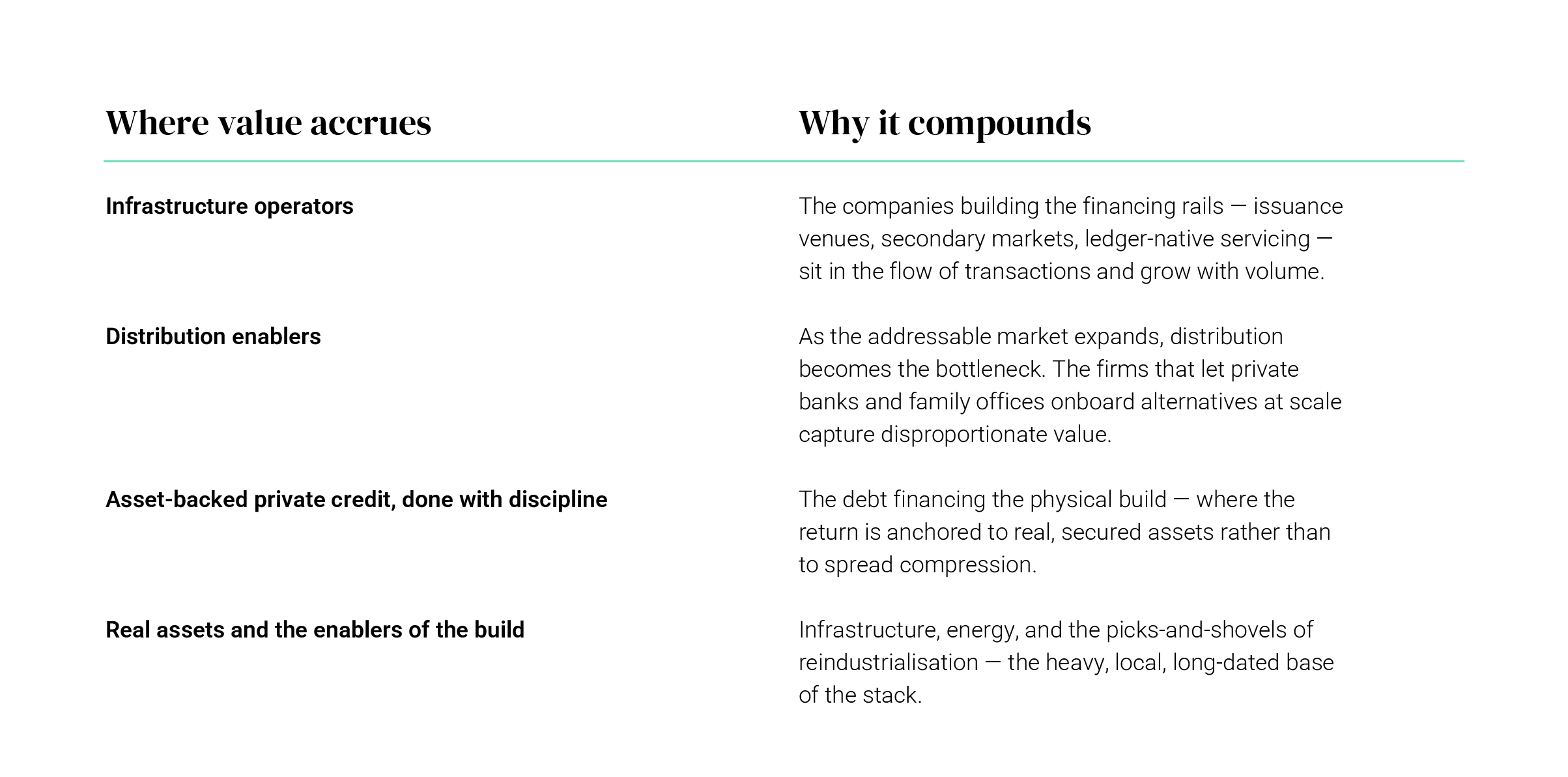

The case for private markets in this cycle is not that they feel smoother. It is that they give an investor ownership of the build itself, through forces public markets do not transmit:

Infrastructure. The literal base of the stack — power, grid, data centres, shipping. This is where the capex physically lands, and it generates contracted, long-duration cash flows that public equity indices do not isolate.

Private credit. A large share of the build is debt-financed. Global private credit assets under management have reached roughly $3 trillion, with insurance and retail-linked capital now meaningful contributors. The opportunity is real — and so is the discipline it demands. In a cycle this flooded with capital, the line between durable exposure and froth runs through the quality of the underlying asset backing. Real assets, properly secured, are the whole game.

Pre-IPO and late-stage equity. The super-cycle's flagship companies are compounding privately, at extraordinary scale, long before they list — if they list at all. The headline-grabbing public offerings arrive only after most of the value has already been created in private hands. The access window that matters is the private one.

Secondaries. When investors in long-dated private positions need liquidity, the secondary market provides it. This is the flow layer of private markets — and the part that most directly mirrors the macro shift from stock to flow.

Set this against the public-market backdrop. The large-cap technology complex that led the last cycle is gradually de-rating as it shifts from capital-light to capital-heavy: the most prominent AI name now trades at roughly 25 times forward earnings, down from a three-year average closer to 32. The index that carried the last decade is top-heavy and, in places, cooling. Owning the physical build — the credit, the infrastructure, the private equity in the companies doing the building — is a genuinely different source of return: driven by fundamentals and active ownership, not by the re-rating of a public multiple.

Private markets are not a quieter version of public ones. They are a complementary engine, powered by different forces. The structural case for holding them in more portfolios was already strong. A decade defined by this kind of spending does not weaken it. It makes it louder, and more urgent than it has been in years.

The capital is concentrating in the investors who were locked out

The returns from financing the super-cycle will accrue disproportionately to owners of capital — and that capital is concentrating in precisely the investor base that infrastructure, not appetite, has historically excluded.

The wealth data is striking. The number of US households with more than $30 million in assets has reached roughly 430,000; those above $100 million number more than 70,000. Increasingly, this wealth belongs not to a narrow technology-and-finance elite but to owners of mid-market and regional businesses — and it is held disproportionately in equities and company stakes rather than real estate, which is exactly why it has compounded faster than average wealth through a decade of rising markets.

This cohort — family offices, private banks, professional investors, the next generation of principals — is the natural financier of a private-markets super-cycle. They want the exposure. What has kept them out is not capital and not conviction; it is operational friction. And that returns us to a parallel I have written about before. In 1865, the economist William Stanley Jevons observed that as steam engines grew more efficient, coal consumption did not fall — it surged, because efficiency unlocked so many new uses that total demand overwhelmed every per-unit saving. When the marginal cost of distributing, servicing and administering private investments collapses — as a shared system of record and an automated system of orchestration allow it to — the market does not stay the same size. It expands to include every professional investor the old cost structure priced out. By one estimate, some $80 trillion in professional wealth remains structurally under-exposed to private assets today. Not by choice. By operational constraint.

The super-cycle and the wealth that will finance it are converging on the same room. The decade's real contest is building the rails that let one reach the other.

Where the value accrues — and what we scan for

If a multi-trillion-dollar financing shift is underway, the natural question is where the durable returns sit. When industries undergo infrastructure-driven cost collapses — cloud in software, digital rails in payments — value tends to flow to a recognisable set of positions:

This is the layer we operate in, and the demand we see firsthand is earlier and larger than the public conversation suggests. We are in the middle of this shift in two capacities at once — as builders of institutional-grade market infrastructure, and as active scanners of where the most compelling private opportunities in this space are forming.

The reflex this year will be to pick the theme and buy the stock. It is the familiar move, and in a super-cycle it is not wrong so much as incomplete. The more durable question — the one our research keeps returning to — is who finances the build, and through what plumbing.

The answer points away from the public index and toward private markets: toward the credit and the infrastructure and the private equity that actually fund the physical world, owned by an investor base that is finally being given the rails to reach it. That is where we are spending our attention.

.jpg)

.jpg)